Modèle IS-LM II

TD Introduction à la macroéconomie

2025-05-06

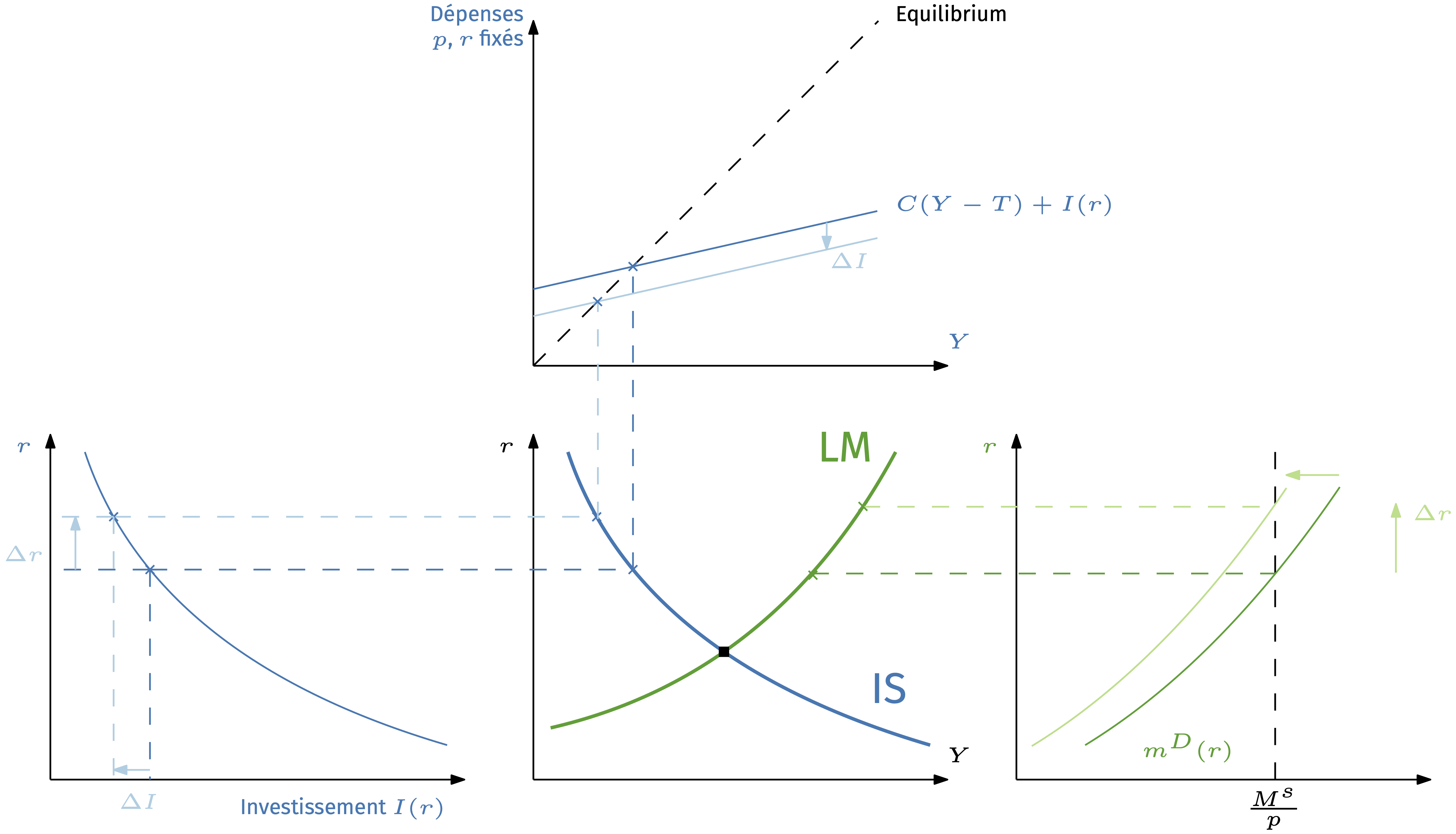

Modèle IS-LM - Une approche plus macro

Modèle IS-LM

#| '!! shinylive warning !!': |

#| shinylive does not work in self-contained HTML documents.

#| Please set `embed-resources: false` in your metadata.

#| standalone: true

#| viewerHeight: 650

from shiny import App, ui, reactive, render_plot

import numpy as np

import matplotlib.pyplot as plt

from scipy.optimize import root_scalar

# -- Functional forms --

# CRRA utility: u(c) = c^(1-sigma)/(1-sigma) => u'(c) = c^(-sigma)

# Production in period 2: F2(K) = A2 * K^alpha2

# Investment condition: F2'(K) = alpha2 * A2 * K^(alpha2-1) = 1 + r => K(r)

# Money demand: mD(Y,i) = Y / i (real money demand)

alpha1, alpha2 = 0.7, 0.3

p1 = 1.0 # price level period 1

def marginal_util(c, sigma):

return c**(-sigma)

def K_of_r(r, A2):

# invert F2'(K)=1+r

return ((1 + r) / (alpha2 * A2))**(1/(alpha2 - 1))

# IS: for a given Y, solve u'(c1) - beta*(1+r)*u'(c2) = 0, where c1=Y-K, c2=F2(K)

def compute_i_IS(Y, beta, A, A2, pi, sigma):

def f_root(r):

K = K_of_r(r, A2)

c1 = Y - K

c2 = A2 * K**alpha2

return marginal_util(c1, sigma) - beta*(1+r)*marginal_util(c2, sigma)

# find bracket [r_lo, r_hi] where f_root changes sign

r_vals = np.linspace(-0.9, 10, 200)

f_vals = [f_root(r) for r in r_vals]

bracket = None

for i in range(len(r_vals)-1):

if f_vals[i] * f_vals[i+1] < 0:

bracket = (r_vals[i], r_vals[i+1])

break

if bracket is None:

# fallback to secant if no bracket found

sol = root_scalar(f_root, x0=0.1, x1=1.0, method='secant', maxiter=100)

else:

sol = root_scalar(f_root, bracket=bracket, method='bisect', maxiter=100)

r_star = sol.root

return r_star + pi

# LM: solve M_s/p1 - Y/i = 0 => i = Y * p1 / M_s

def compute_i_LM(Y, M_s):

return Y * p1 / M_s

# -- UI --

app_ui = ui.page_fluid(

ui.h2("IS-LM with Exact Equations"),

ui.layout_sidebar(

ui.sidebar(

ui.input_slider("A", "Productivity A (F1 scale):", min=0.5, max=2.0, value=1.0, step=0.1),

ui.input_slider("A2", "Optimism A2 (F2 scale):", min=0.5, max=2.0, value=1.0, step=0.1),

ui.input_slider("beta", "Discount β:", min=0.1, max=1.0, value=0.98, step=0.01),

ui.input_slider("sigma","CRRA σ:", min=0.5, max=5.0, value=2.0, step=0.1),

ui.input_slider("Ms", "Money Supply M^S:", min=0.5, max=5.0, value=1.0, step=0.1),

ui.input_slider("pi", "Inflation π:", min=0.0, max=0.5, value=0.02, step=0.01),

ui.input_action_button("reset", "Reset Defaults")

),

ui.card(

ui.card_header("IS & LM Diagram"),

ui.card_body(ui.output_plot("plot", height="600px"))

)

)

)

# -- Server --

def server(input, output, session):

# store initial defaults

DEFAULTS = {

"A": 1.0,

"A2": 1.0,

"beta": 0.98,

"sigma":2.0,

"Ms": 1.0,

"pi": 0.02

}

# reset sliders to initial defaults when button is pressed

@reactive.event(input.reset)

def _reset_inputs():

for name, val in DEFAULTS.items():

session.set_input_value(name, val)

@output

@render_plot()

def plot():

# Base parameters

A0, A20, beta0, sigma0, Ms0, pi0 = 1.0, 1.0, 0.98, 2.0, 1.0, 0.02

# Current

A, A2, beta, sigma, Ms, pi = (

input.A(), input.A2(), input.beta(), input.sigma(), input.Ms(), input.pi()

)

# Y grid

Y = np.linspace(0.1, 10, 100)

# Compute curves

i_IS_base = [compute_i_IS(y, beta0, A0, A20, pi0, sigma0) for y in Y]

i_LM_base = compute_i_LM(Y, Ms0)

i_IS_cur = [compute_i_IS(y, beta, A, A2, pi, sigma) for y in Y]

i_LM_cur = compute_i_LM(Y, Ms)

# Equilibrium for current

eq_diff = np.abs(np.array(i_IS_cur) - np.array(i_LM_cur))

idx = eq_diff.argmin()

Y_eq, i_eq = Y[idx], i_IS_cur[idx]

# Plot

fig, ax = plt.subplots(figsize=(8,6))

# base curves

ax.plot(Y, i_IS_base, '--', color='gray', alpha=0.5, label='IS (base)')

ax.plot(Y, i_LM_base, '--', color='gray', alpha=0.5, label='LM (base)')

# current curves

ax.plot(Y, i_IS_cur, '-', color='crimson', label='IS (current)')

ax.plot(Y, i_LM_cur, '-', color='navy', label='LM (current)')

# equilibrium

ax.plot(Y_eq, i_eq, 'ko')

ax.axhline(i_eq, linestyle='--', color='black')

ax.axvline(Y_eq, linestyle='--', color='black')

ax.text(Y_eq, i_eq, f' (Y*, i*)=({Y_eq:.2f},{i_eq:.2f})')

ax.set_xlabel('Output Y')

ax.set_ylabel('Interest rate i')

ax.set_title('Exact IS-LM Curves')

ax.legend()

ax.grid(True)

return fig

app = App(app_ui, server)![]()